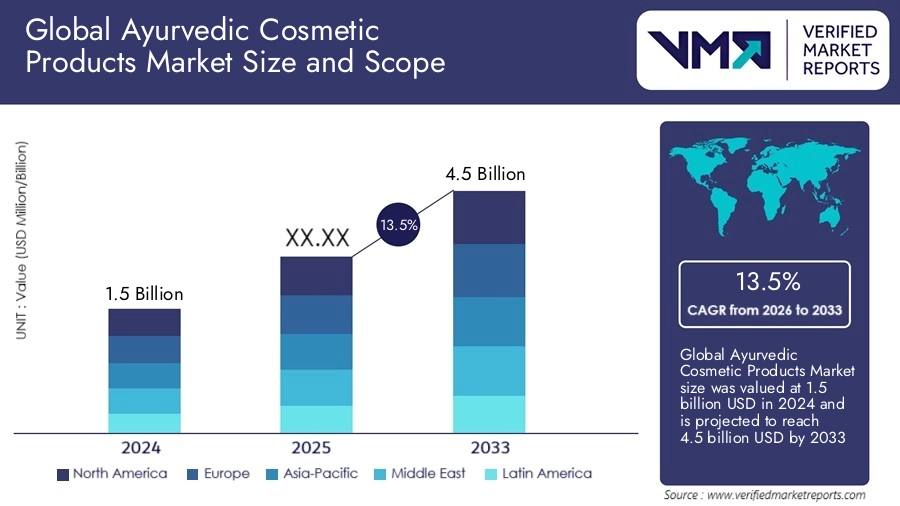

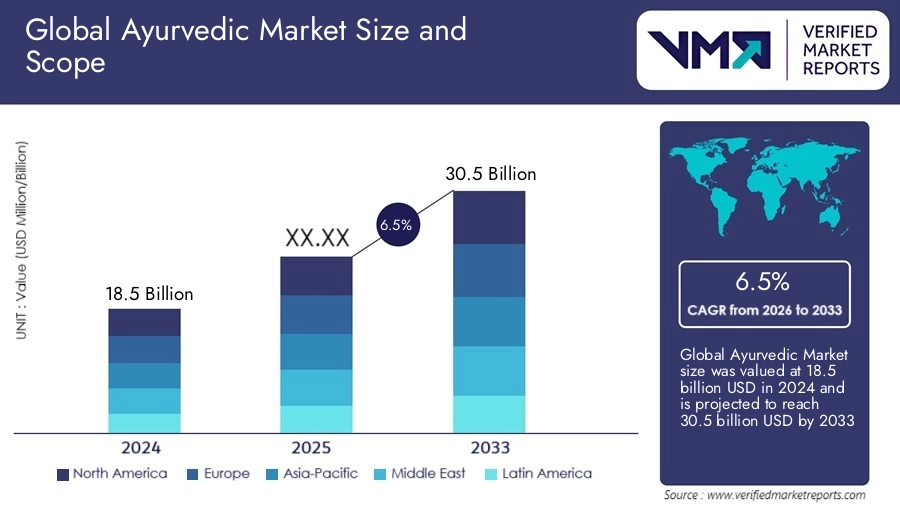

Introduction

The top companies in Ayurvedic industry are driving a powerful transformation in global healthcare, blending traditional herbal science with modern research and commercialization strategies. The market is witnessing robust expansion, with an estimated valuation of USD 12-15 billion in 2024 and projected to grow at a CAGR of 14-16% through 2034. Rising consumer preference for natural remedies, increasing awareness of preventive healthcare, and regulatory support for herbal medicine are accelerating growth.

![Top Ayurvedic Trends- Verified Market Reports [2025]](https://www.verifiedmarketreports.com/images/blogs/11-23/Top_10_Ayurvedic_Companies[1].png)

Key drivers include the shift toward clean-label products, integration of Ayurveda into mainstream healthcare, and aggressive global expansion strategies by leading players. Competition is intensifying as legacy brands and emerging innovators compete on product efficacy, distribution reach, and digital transformation. Strategic positioning, innovation pipelines, and supply chain integration are now critical differentiators shaping long-term market leadership.

Key Insights

- Leading company: Dabur India Ltd. dominates with strong brand equity and diversified portfolio.

- Fastest-growing player: Patanjali Ayurved, driven by aggressive pricing and mass-market penetration.

- Dominant region: Asia-Pacific leads due to cultural roots and large consumer base.

- Market structure: Moderately fragmented with a mix of legacy brands and regional players.

- Key trend: Rapid shift toward scientific validation and global standardization of Ayurvedic formulations.

Competitive Landscape Overview

The Ayurvedic sector exhibits a semi-fragmented competitive structure, where a handful of established brands dominate organized retail, while numerous regional players cater to localized demand. Entry barriers remain moderate, primarily due to regulatory requirements, sourcing challenges for high-quality herbs, and the need for clinical validation in global markets.

Competitive intensity is increasing as companies invest heavily in R&D, branding, and international certifications. Pricing strategies vary significantly premium brands focus on clinically validated, export-grade products, while mass-market players leverage affordability to drive volume.

Innovation is a key battleground. Companies are integrating modern extraction technologies, AI-based formulation research, and digital health platforms to enhance product efficacy and consumer engagement. Additionally, e-commerce and D2C channels are reshaping distribution dynamics, enabling smaller brands to scale rapidly.

Strategic collaborations, especially with healthcare institutions and global distributors, are further intensifying competition and accelerating market consolidation trends.

Top Companies in the Market

Dabur India Ltd.

- Overview: A flagship Ayurvedic brand with a diversified FMCG and healthcare portfolio.

- Headquarters: Ghaziabad, India

- Founded: 1884

- Revenue: ~$1.5–2 billion

- Core segments: Healthcare, personal care, foods

- Key offerings: Chyawanprash, herbal supplements, skincare

- Strategic developments: Expansion into international markets and digital health platforms

- Positioning: Market leader

- Why it matters: Strong brand trust and global reach position it as a benchmark for scalability.

Baidyanath

- Overview: Legacy Ayurvedic manufacturer with deep-rooted authenticity.

- Headquarters: Kolkata, India

- Founded: 1917

- Revenue: ~$300-400 million (estimated)

- Core segments: Ayurvedic medicines, health tonics

- Key offerings: Classical formulations, herbal tonics

- Strategic developments: Strengthening retail and export footprint

- Positioning: Established challenger

- Why it matters: Strong heritage credibility drives consumer loyalty.

Hamdard Laboratories

- Overview: A major player blending Unani and Ayurvedic solutions.

- Headquarters: New Delhi, India

- Founded: 1906

- Revenue: ~$200-300 million

- Core segments: Herbal medicine, wellness products

- Key offerings: Health tonics, digestive solutions

- Strategic developments: Product diversification and R&D focus

- Positioning: Niche innovator

- Why it matters: Strong research-backed formulations enhance credibility.

Patanjali Ayurved

- Overview: Disruptor with mass-market accessibility and aggressive expansion.

- Headquarters: Haridwar, India

- Founded: 1997

- Revenue: ~$1-1.2 billion

- Core segments: FMCG, healthcare, food products

- Key offerings: Herbal medicines, personal care, packaged foods

- Strategic developments: Retail expansion and supply chain integration

- Positioning: High-growth challenger

- Why it matters: Price disruption reshaped competitive dynamics.

Himalaya Drug Company

- Overview: Science-driven herbal healthcare brand with global presence.

- Headquarters: Bengaluru, India

- Founded: 1930

- Revenue: ~$500-700 million

- Core segments: Pharmaceuticals, personal care

- Key offerings: Herbal medicines, skincare, nutraceuticals

- Strategic developments: Clinical research expansion

- Positioning: Global leader

- Why it matters: Strong scientific validation supports global expansion.

Zandu Pharmaceutical Works Ltd.

- Overview: Established brand with wide product portfolio.

- Headquarters: Mumbai, India

- Founded: 1910

- Revenue: ~$100-200 million

- Core segments: Ayurvedic medicines, OTC products

- Key offerings: Pain relief, digestive solutions

- Strategic developments: Brand repositioning and product innovation

- Positioning: Established player

- Why it matters: Strong recall in traditional OTC segment.

Saptarishi Ayurveda Ltd.

- Overview: Focused herbal medicine manufacturer.

- Headquarters: India

- Founded: 1981

- Revenue: ~$50-100 million

- Core segments: Herbal supplements

- Key offerings: Ayurvedic formulations

- Strategic developments: Expansion in regional markets

- Positioning: Niche player

- Why it matters: Focused portfolio enables specialization.

Vaidyaratnam Oushadhalaya

- Overview: Heritage institution with strong traditional expertise.

- Headquarters: Thrissur, India

- Founded: 1902

- Revenue: ~$50-80 million

- Core segments: Ayurvedic medicine and treatments

- Key offerings: Classical formulations

- Strategic developments: Institutional partnerships

- Positioning: Heritage specialist

- Why it matters: Deep-rooted expertise enhances authenticity.

Arya Vaidya Pharmacy (Coimbatore) Ltd.

- Overview: Integrated healthcare provider with treatment services.

- Headquarters: Coimbatore, India

- Founded: 1902

- Revenue: ~$80-120 million

- Core segments: Medicines, wellness services

- Key offerings: Therapeutic treatments, herbal products

- Strategic developments: Expansion of wellness centers

- Positioning: Integrated provider

- Why it matters: Service-based model creates differentiation.

Kerala Ayurveda Limited

- Overview: Publicly listed Ayurvedic company with global reach.

- Headquarters: Aluva, India

- Founded: 1974

- Revenue: ~$30-60 million

- Core segments: Healthcare, wellness, products

- Key offerings: Herbal medicines, spa services

- Strategic developments: International expansion

- Positioning: Emerging global player

- Why it matters: Strong export focus drives future growth.

Download Sample Report Now: Global Ayurvedic Market Size And Forecast [2024-2030]

Comparative Analysis

The competitive comparison highlights a clear divide between legacy giants and emerging disruptors, with scale, innovation, and pricing strategies defining leadership positioning.

| Company | Revenue | Key Strength | Region | Strategy |

|---|---|---|---|---|

| Dabur | High | Brand equity | Global | Diversification |

| Patanjali | High | Pricing | India | Mass expansion |

| Himalaya | Medium | R&D | Global | Clinical validation |

| Baidyanath | Medium | Heritage | India | Trust-driven |

Leaders leverage brand and scale, while challengers compete through affordability and innovation.

Market Share Analysis

The market demonstrates a moderate concentration, with top players accounting for approximately 45-55% of total revenue. Dabur and Patanjali lead in volume-driven segments, while Himalaya dominates premium and export categories.

Regional players collectively contribute a significant share, reflecting strong local demand and fragmented supply chains. Emerging brands are gaining traction through digital-first strategies and niche product positioning.

The increasing entry of startups and wellness-focused brands is intensifying competition, particularly in urban and international markets.

Recent Developments

- Product innovation: Launch of clinically tested herbal supplements

- Partnerships: Collaborations with global distributors

- Expansion: Entry into North America and Europe

- Digital transformation: Growth of D2C and e-commerce channels

- Investments: Increased R&D spending for validation studies

Strategic Insights

The Ayurvedic sector is entering a phase of global institutionalization, where companies that successfully combine traditional knowledge with scientific validation will emerge as long-term leaders. Dabur and Himalaya are well-positioned due to their strong R&D pipelines and international presence.

Patanjali’s disruptive pricing strategy will continue to influence competitive dynamics, but sustaining growth will require quality standardization and global compliance.

Future disruption is expected from digitally native brands leveraging AI for formulation and personalized wellness solutions. Additionally, integration with modern healthcare systems and insurance frameworks could unlock new revenue streams.

Investment opportunities lie in companies focusing on export-oriented growth, clinical research, and premium product positioning. The convergence of Ayurveda with nutraceuticals and functional foods will further expand the addressable market.

Conclusion

The Ayurvedic sector is evolving into a high-growth, innovation-driven ecosystem with strong global potential. Established leaders continue to dominate through brand strength and distribution, while emerging players are reshaping the landscape with agility and innovation.

As consumer demand for natural healthcare accelerates, companies that invest in research, digital transformation, and global expansion will define the next phase of growth.

Request a sample report, connect with our analysts, or explore full market insights to stay ahead in this rapidly evolving sector.

Frequently Asked Questions

Q1. Who are the top companies in Ayurvedic?

Leading players include Dabur, Patanjali, Himalaya, Baidyanath, and Zandu, supported by several regional and niche innovators driving market expansion.

Q2. Which company holds the largest market share?

Dabur India Ltd. is widely considered the market leader due to its diversified portfolio and strong global presence.

Q3. Which company is growing the fastest?

Patanjali Ayurved is among the fastest-growing, driven by aggressive pricing and large-scale distribution strategies.

Q4. What strategies define success in this market?

Key strategies include product innovation, clinical validation, digital distribution, and international expansion.

Q5. Which region dominates the market?

Asia-Pacific leads the market, supported by cultural adoption and strong domestic demand, while global markets are rapidly emerging.